Life Insurers: Major Players in the Private Credit Market

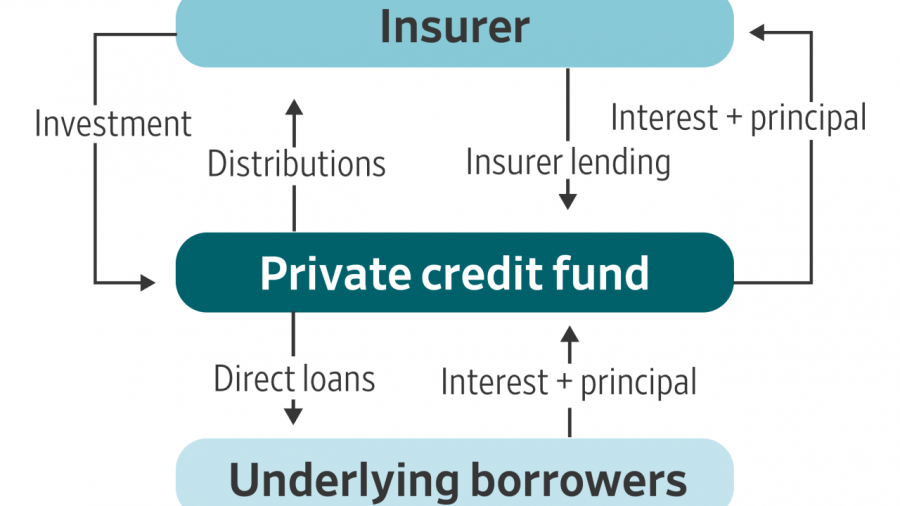

As the financial landscape evolves, life insurers are taking on a dual role in the realm of private credit. Not only are these institutions significant investors in private credit funds, but they are also emerging as major lenders to these very funds, creating a complex web of financial interdependence.

The Growing Influence of Life Insurers

According to recent data from Clearwater Analytics, approximately one-quarter of life insurance companies that have stakes in private credit funds are also providing loans to those funds. This trend highlights a pivotal shift in how these institutions operate within the financial ecosystem.

Understanding Private Credit

Private credit refers to non-bank lending, where funds are raised from investors to lend directly to companies or projects, bypassing traditional banks. This sector has seen explosive growth in recent years, driven by the need for alternative financing solutions in a low-interest-rate environment.

Life Insurers: A Dual Role

Life insurers have traditionally been seen as conservative investors, focusing on long-term, stable returns to meet their policyholder obligations. However, with the increasing demand for private credit, these companies are adapting their strategies.

By not only investing in private credit funds but also lending directly to them, life insurers are enhancing their exposure to potentially lucrative returns. This dual role allows them to diversify their portfolios while supporting the growth of private enterprises that may struggle to secure financing through conventional banking channels.

Benefits of Being a Lender

There are several advantages for life insurers that choose to lend to private credit funds:

- Enhanced Yield: Life insurers can command higher interest rates as lenders to private credit funds compared to traditional fixed-income investments.

- Portfolio Diversification: By participating as lenders, insurers can further diversify their investment portfolios, reducing overall risk.

- Strategic Relationships: Lending to private credit funds fosters closer relationships with fund managers, providing insurers with insights into emerging opportunities and trends.

- Meeting Policyholder Needs: Increased returns from private credit can help insurers meet their obligations to policyholders, especially in a low-yield environment.

Risks and Considerations

While the potential rewards are significant, life insurers must also navigate various risks associated with lending to private credit funds. These include credit risk, market risk, and liquidity risk. Insurers must conduct thorough due diligence to assess the creditworthiness of the funds they choose to support.

Looking Ahead

The role of life insurers in the private credit market is likely to expand further as they continue to seek innovative ways to enhance returns and manage risk. As private credit funds become an integral part of the financial landscape, life insurers will play a crucial role in shaping this sector.

In conclusion, life insurers are not just passive investors in private credit; they are becoming active lenders, significantly influencing the dynamics of the market. As this trend evolves, it will be essential for industry stakeholders to monitor the implications of life insurers’ increasing involvement in private credit lending.